Rethinking Retirement Income: Beyond the 60/40 Portfolio

- John Macy

- Dec 10, 2025

- 5 min read

Updated: 4 days ago

Written by John Macy, Financial Coach, MBA, Retirement Income Certified Professional® (RICP)

Introduction

Many people have saved diligently for retirement for decades, and they might have accumulated a nice portfolio of investments, but then they wonder "How do I create a 'retirement paycheck' from this portfolio?"

For decades, the “standard advice” for retirement has looked something like this:👉 Hold a balanced portfolio of low-cost index funds (maybe 60% stocks / 40% bonds, or perhaps 70% stocks / 30% bonds)

👉 Withdraw around 4% per year (adjusted for inflation each year) to cover living expenses

It’s simple, it’s popular, and for many retirees, it works.

But there are a couple of catches…

The 60/40 Portfolio May not be as Diversified as you Think

Over the last 20-30 years, research has demonstrated that a portfolio composed only of stocks and bonds may not be as diversified as people think. In certain economic climates (such as 2022) stocks and bonds can both decline significantly at the same time.

Alternative investments (e.g., managed futures, precious metals, commodities, real estate, etc.) can provide much better diversification and are often part of an "all-weather" portfolio. The chart below from BlackRock illustrates how increased diversification using alternatives can reduce the volatility of your portfolio while increasing the total returns.

This article explains how you can more effectively (and even simply) diversify your portfolio.

Sequence of Returns Risk

Sequence of return risk is the risk that the timing of investment returns — especially early in retirement — has a large impact on how long your portfolio lasts. An investor who earns an average return of 10% per year but who experiences poor market returns in the first decade of retirement while also withdrawing money from the portfolio can run out of funds much sooner than another investor who earns the same average return but experiences those losses later in retirement.

If the stock market performs poorly in the decade right before or after you retire, your portfolio could shrink faster than expected — just when you need it most. This is especially true if you are selling large quantities of stock shares during those downturns. Even if the market recovers later, your withdrawals during the downturn will leave you with fewer shares of stock to benefit from the rebound.

Retirees Prefer Steady Income

On top of that, research shows that retirees are more willing to spend regular guaranteed sources of income (such as Social Security, pensions, annuities) than from their portfolio. Retirees spend about 80% of guaranteed lifetime income (e.g., SS, pensions, annuities) and only about 50% of their other investment income (“Retirees Spend Lifetime Income, Not Savings” by David Blanchett and Michael Finke (December 2024)). Other studies found that retirees preferred spending dividends and bond interest, and viewed the sale of stock as a last resort (“The Dividend Effect on Consumption” by Malcolm Baker, Stefan Nagel, and Jeffrey Wurgler (2006)). Personal psychology, priorities, and preferences are important factors in the decision about how to construct a retirement income portfolio.

Alternative Retirement Income Strategies

If you want steadier, more predictable cash flow, here are some options worth exploring:

Income Strategy | Average Current Yield | The Key Benefit | Tax Treatment |

Fixed Immediate (or Deferred) Income Annuities | Varies with age & interest rates | Creates a guaranteed income foundation for life. | If purchased with qualified funds (IRA) then ordinary income; if purchased with taxable funds, then ordinary income on a portion of the distribution based on an "exclusion ratio" |

Rental Properties | Varies | Monthly cash flow + potential for appreciation. | Ordinary Income after deducting expenses & depreciation, but typically qualifies for 20% QBI deduction |

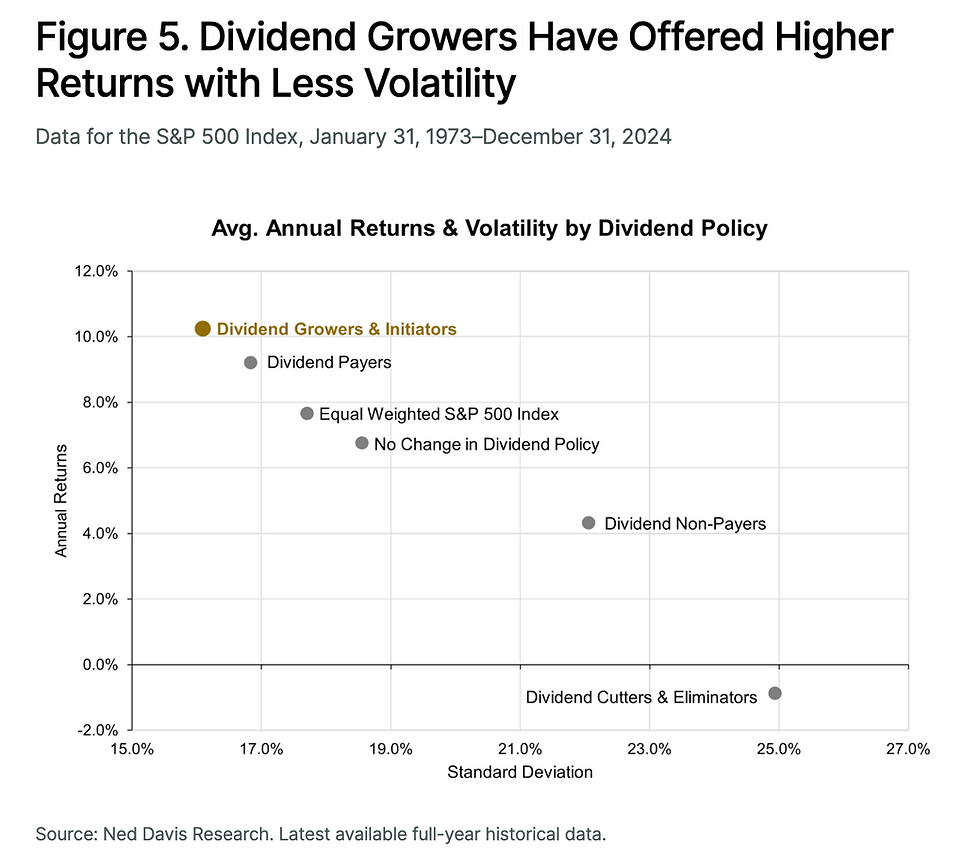

Dividend Growth Stocks | 2.5% – 5% | Fairly reliable income that can grow faster than inflation. ETFs include SCHD, DGRO, VIG, VIGI, DIVI, and LVHI. | Often qualified dividends, taxed at lower rates similar to long-term capital gains |

Preferred Stocks | ~5.5% | A fixed-income alternative to corporate bonds. Typically pay more than bonds. | Often qualified dividends, taxed at lower rates similar to long-term capital gains |

Real Estate Investment Trusts (REITs) | ~4–5% | Relatively high payout from commercial real estate. Examples include O, PLD, REXR, WPC, and the ETF VNQ. | Ordinary Income (High Tax Drag), but typically qualify for 20% QBI deduction |

Master Limited Partnerships (MLPs) | ~7.8% | Income from essential energy/infrastructure assets. Examples include EPD, ET, BIP. | Usually fairly tax efficient but more complicated K-1 Tax Forms |

Business Development Companies (BDCs) | 9–10% | High yields from lending to small and mid-sized businesses. Examples include MAIN, ARCC, FDUS. | Non-Qualified Dividends (Ordinary Income Tax Rates) |

Another important benefit from investing in these options listed above is that they can further diversify your portfolio, reducing overall volatility and risk. Which of these options is right for you will depend on a number of factors including your risk tolerance.

A Critical Warning

Don't just chase the highest yield! Investments yielding much higher than average in each category above tend to carry much higher risk than their lower-yielding peers, resulting in lower long-term risk-adjusted performance. For dividend growth stocks and REITs, consider buying an ETF to invest in a safer, more diversified portfolio. For each of the categories above research and due diligence is necessary before investing.

Also note that dividends (or interest) are a component of total return (capital gains are the other component), and in the end, total return is ultimately what matters for wealth creation and wealth preservation.

When thinking about risk, it is important to distinguish between income volatility and price volatility. For example, BDCs, MLPs, and REITs may have high price swings (volatility), but if they maintain their dividend payouts, the income remains stable for the retiree. Understanding this difference is key to 'rethinking' the 60/40 model.

Because assets like BDCs and REITs are taxed at ordinary income rates, placing them in their proper asset location (preferably in a tax-deferred account like an IRA) is critical to maximizing your after-tax retirement paycheck. Learn more about proper asset location here.

The Bottom Line: Building an Income Foundation

There’s no one-size-fits-all retirement income plan. A traditional 60/40 portfolio of stock index funds works for some, but additional alternatives can provide greater diversification, higher, steadier cash flow, increase your willingness and ability to spend — and may reduce stress about selling assets in down markets.

Well-designed retirement plans often blend multiple strategies. Use reliable income sources (Social Security, pension, annuities, interest, dividends) to cover your essential needs, and use more growth-oriented investments to cover your discretionary spending. This minimizes risk while maximizing your lifetime financial security. Read our guide to creating a secure retirement income foundation.

At FlourishingPath Financial Coaching, I help clients explore income strategies that match their goals, risk tolerance, and lifestyle. Contact me or visit www.flourishingpathfinancial.com/book-online if you would like friendly, expert, personalized assistance in planning your retirement.

Author: John Macy, MBA, RICP®

John Macy is a professional financial coach and the founder of FlourishingPath Financial Coaching. With over six years of experience as a financial coach, John helps pre-retirees and retirees design resilient portfolios and income streams for their next act. Read his full story here.

Comments