Can You Live on Dividends and Interest in Retirement?

- John Macy

- Dec 10, 2025

- 5 min read

Updated: 2 days ago

Written by John Macy, Financial Coach, MBA, Retirement Income Certified Professional® (RICP)

It sounds like financial freedom, right? Building a portfolio with a consistent 4%+ dividend (and interest) yield, funding your lifestyle, and never touching your principal.

In theory, it's possible! If your income consistently covers expenses, you preserve your nest egg indefinitely. And possibly enjoy a less stressful retirement.

What Should Dividend Investors Consider?

🔥 INFLATION EROSION: Your living costs will rise. Will your dividends keep up? Many companies raise payouts more slowly than inflation, quietly shrinking your purchasing power over the years. Look for Dividend Growth stocks, not just high yield! And ideally, your portfolio should generate more income than you need, allowing you to reinvest the surplus. This helps your future dividend stream grow and keep pace with inflation.

💸 LARGER PORTFOLIO MAY BE REQUIRED (If your portfolio yield is less than 4%): To generate an income of, say, $50,000/year from a 3% yield, you need a $1.67 Million portfolio. $50K/year from a 2% yield requires a $2.5 Million portfolio. A "Total Return Investing" approach (focusing more on growth and selling some shares as needed to withdraw 4% or 5% each year) requires a smaller initial balance ($1.25 million with a 4% withdrawal rate and $1.0 million with a 5% withdrawal rate).

⚠️ DIVIDEND CUTS ARE REAL: Even once-strong dividend-paying companies (think AT&T, GE, 3M, British Petroleum) face challenges and can reduce or suspend dividends overnight. Diversification is non-negotiable. Never let your income rely too heavily on a couple of stocks or only one or two sectors. Invest in at least 4 or 5 different sectors or preferably dividend-focused Exchange Traded Funds (ETFs) that are well diversified (e.g., SCHD, DGRO, LVHI, DIVI).

🚫 BEWARE THE HIGH-YIELD TRAP: Chasing 7%, 8%, or 10% yields is tempting, but often means higher risk. A high dividend yield (or interest rate) frequently signals that the payout is unsustainable or the company is struggling.

🧠 Flexibility is Key: Delaying Social Security until age 67-70 is a powerful strategy, even if it means you must occasionally sell a few shares to "bridge the gap" for a few years while you wait for SS to start. Selling shares is NOT a failure if it's part of a sound total return plan! For additional insights on Social Security see these articles: "When is the Best Time to Claim SS?" and "How to Create an Income Bridge to Delay SS".

💰 LARGE ENDING PORTFOLIO LIKELY: Focusing on "never touching the principal" means you're intentionally accepting a lower standard of living in retirement. Your heirs might enjoy your wealth more than you do.

Dividend Growth vs. High Yield

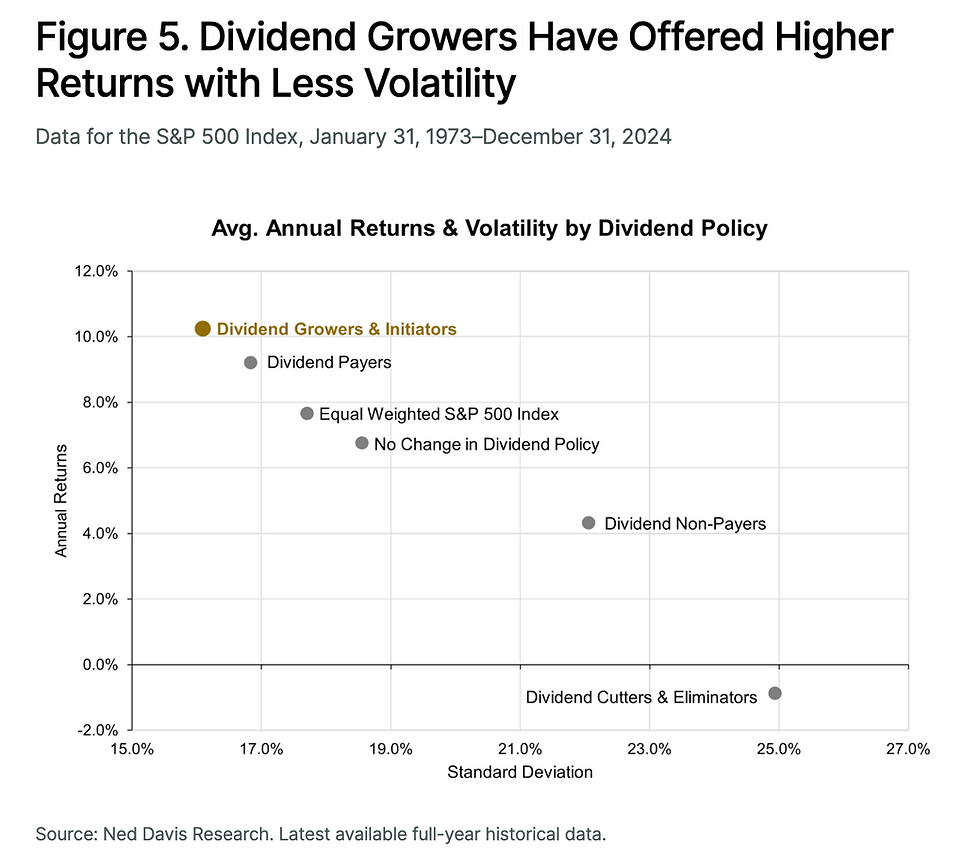

Dividend Growth involves investing in companies with a track record of increasing dividend payouts annually (for example, stocks known as Dividend Aristocrats which have increased their dividend/share payout every year for 25 years), which helps your income keep pace with inflation. It is very possible to invest in high quality dividend growth stocks with dividend yields ranging from 2-5%. There are also some categories of stocks such as Real Estate Investment Trusts (REITs), Business Development Companies (BDCs), and Master Limited Partnerships (MLPs) which routinely pay out dividends in the 5-8% range. As mentioned above, outside of REITs, BDCs, and MLPs, chasing stocks with high yields above 5% often signals a 'Value Trap' where the payout is unsustainable.

How Large a Portfolio Do You Need to Live on Dividends and Interest?

As noted above, living exclusively on dividends and interest may require a fairly large portfolio. The table below illustrates the size of the portfolio required based on the amount of income that you desire from the portfolio and the dividend/interest yield generated by that portfolio (generally correlated with the risk of the portfolio).

Annual Income Goal* | 2% Yield** (Portfolio Size) | 3% Yield** (Portfolio Size) | 4% Yield** (Portfolio Size) | 5% Yield** (Portfolio Size) |

$40,000 | $2 million | $1.33 million | $1.0 million | $800,000 |

$60,000 | $3 million | $2.0 million | $1.5 million | $1.2 million |

$80,000 | $4 million | $2.67 million | $2.0 million | $1.6 million |

$100,000 | $5 million | $3.33 million | $2.5 million | $2.0 million |

*Note: Annual Income Goal above is in addition to any guaranteed income sources such as pensions, Social Security, annuities, etc.

**Note: Yield above is the weighted average blended dividend/interest yield across all of the stock, bond, and alternative holdings in your portfolio.

Scenario Comparison: "Dividend Growth" vs. "Total Return"

Below is a 10-year scenario comparing two investors pursing different strategies: "Dividend Growth" Irene and "Total Return" Tom.

Portfolio Assumptions:

Portfolio Mix: 60% Stocks / 40% Bonds ($1M Start).

Irene's 60% Stock Portfolio Composition: 25% each of SCHD, DGRO, LVHI, and DIVI ETFs

Tom's 60% Stock Portfolio Composition: 100% Total US Stock Index fund

Irene and Tom's 40% Bond Portfolio Composition: 100% Total US Bond Index fund

Irene's initial Stock Portfolio Dividend Yield: 3.78% (historical average of 4 ETFs)

Irene's Stock Portfolio Dividend Growth Rate: 8.05% (historical average of 4 ETFs)

Tom's Stock Portfolio Total Return: 10.9% (historical average)

Bond Yield: 3.5% (Total US Bond Index).

Spending Goal: $40,000 in Year 1, increasing 3% annually for inflation.

Shortfall/Surplus Policy: If dividends/interest don't cover the goal, principal is sold. When there is a surplus of dividends/interest, it is reinvested back into the portfolio.

10-Year Comparison Between "Dividend Growth" Irene and "Total Return" Tom

Year | Income Needed (3% Inflation) | "Dividend Growth" Irene | "Total Return" Tom |

1 | $40,000 | Shortfall: -$3,320 (Sells shares) | Met Goal (Sells shares) |

3 | $42,436 | The Crossover: Dividends now $42,800 | Met Goal (Sells shares) |

5 | $45,020 | Surplus: +$4,650 (Reinvested) | Met Goal (Sells shares) |

10 | $52,190 | Surplus: +$21,400 (Reinvested) | Met Goal (Sells shares) |

Ending Value | $1,515,000 | $1,282,000 |

For the assumptions used, both strategies were successful in producing the annual income required, but "Dividend Growth" Irene had a larger ending portfolio value than "Total Return" Tom. Of course, varying the assumptions would result in different outcomes. For example, substituting Vanguard's dividend appreciation ETF VIG instead of the blended mix of SCHD, DGRO, LVHI, and DIVI above for Irene would result in very similar outcomes between Irene and Tom in terms of ability to produce required annual income and ending portfolio value.

What this scenario comparison illustrates is that both strategies have merit and can be successfully implemented by retirees. It also illustrates that there is more than one way to implement the "Dividend Growth" strategy, and the choice of implementation method will affect the retiree's outcome. The key is to understand the pitfalls and weaknesses of each strategy, mitigate those weaknesses (for example by ensuring adequate diversification and not chasing high yield or ultra risky growth stocks), and select the strategy that fits your situation and personality.

THE BOTTOM LINE

Living off dividends alone can be a successful retirement strategy, but only when executed with smart diversification, an intentional plan for inflation, and a clear understanding of the risks. A sustainable income strategy balances immediate yield, quality, growth, and flexibility.

Ready to design a retirement income plan that lasts and adapts to any market? Let’s build a resilient retirement income plan together.

Visit www.flourishingpathfinancial.com/book-online to book a free Discovery Session or send me a message if you would like friendly, expert assistance in building your retirement income plan.

Author: John Macy, MBA, RICP®

John Macy is a professional financial coach and the founder of FlourishingPath Financial Coaching. With over six years of experience as a financial coach, John helps pre-retirees and retirees design resilient portfolios and income streams for their next act. Read his full story here.

Comments