How Do Dividends & Interest Fit Into the 4% Rule?

- John Macy

- Dec 10, 2025

- 4 min read

Updated: 2 days ago

Written by John Macy, Financial Coach, MBA, Retirement Income Certified Professional® (RICP)

If you have read about retirement income strategies, you have probably heard of the 4% Rule — the classic guideline for how much you can safely withdraw from your investments each year in retirement. But what exactly does it mean, and how do dividends and interest fit into that rule? Let’s unpack it.

The Origins of the 4% Rule

The 4% Rule traces back to financial planner Bill Bengen’s 1994 study, which analyzed historical U.S. market returns to determine a sustainable withdrawal rate for retirees. Bengen found that retirees who withdrew 4% of their portfolios in the first year of retirement, then increased that amount annually to keep up with inflation, could expect their savings to last at least 30 years — even through some of the worst market conditions, including the Great Depression and the 1970s stagflation period.

This conclusion was later supported and expanded by the well-known Trinity Study (1998), conducted by three finance professors from Trinity University. Their research tested multiple withdrawal rates and asset allocations across different time periods and confirmed that a 4% initial withdrawal rate (from a diversified stock and bond portfolio) offered a very high likelihood of success for 30-year retirements.

Study | Author / Source | Key Finding | Success Metric |

Bengen Study (1994) | Bill Bengen | 4% is the "SAFEMAX" withdrawal rate | 30-year portfolio survival for a 50/50 stock/bond portfolio |

Trinity Study (1998) | Trinity University | Confirmed 4% at various mix levels | 95%+ success for 60/40 portfolios |

Is It Still the 4% Rule — or the 5% Rule?

For decades, the 4% Rule has served as a reliable starting point and “rule of thumb” for retirement planning. However, more recent analyses — incorporating lower expected inflation, longer retirements, and improved portfolio diversification — suggest that retirees today might safely withdraw a bit more, perhaps around 4.5% to 5%, without a significant increase in risk of running out of money over a typical 30-year retirement planning horizon.

That said, future returns are uncertain, so flexibility and annual review remain key to success — no matter which “rule” you start with.

So How Do Dividends & Interest Fit Into Your Withdrawal Strategy?

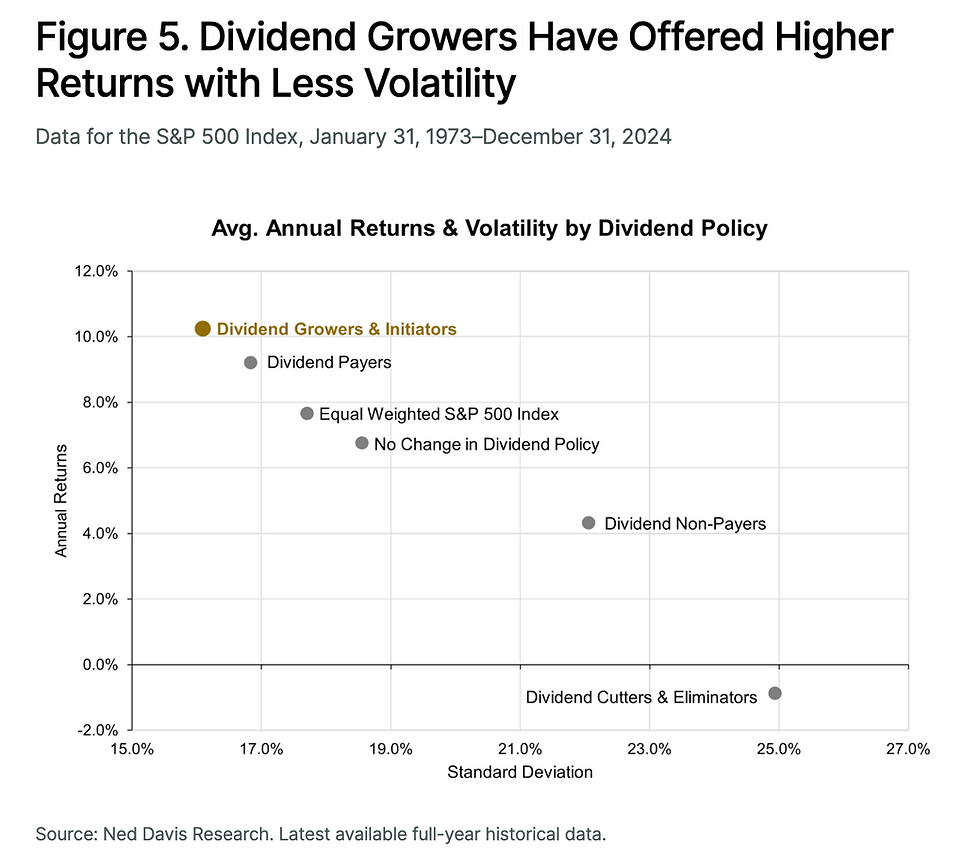

Many retirees choose to focus on earning dividends and interest from their investments because they tend to be more reliable and stable sources of income than depending on selling shares of stock that experience periods of high price volatility. There is nothing wrong with that strategy. In fact, as illustrated in the graphic below, studies have shown that (on average) stocks of companies with regularly growing dividends tend to have higher total returns than companies with flat dividends, declining dividends, or no dividends.

However, a key principle to keep in mind is that dividends and interest are part of an asset’s total return — they are not extra. Every investment’s total return is made up of two components:

Total Return = Dividend/Interest + Price Appreciation (Growth)

Many investors mistakenly assume dividends and interest are on top of their portfolio’s total return. In reality, they are components of it.

Example: If your mutual fund earns a 7% total return in a year, that might include 2% from dividends and 5% from price appreciation.

When applying the 4% Rule (or the 5% Rule, depending on your analysis), you are drawing from the total return — not just from the growth portion or the dividend portion.

Spend Income First in Taxable Accounts

Here is a key tax-efficient withdrawal tip: if you have taxable brokerage accounts, you will pay taxes on dividends and interest every year — whether you spend that income or reinvest it. That means when you are drawing retirement income, it usually makes sense to spend your dividends and interest first before selling shares or pulling money from tax-deferred accounts (like IRAs or 401(k)s).

Otherwise, you could end up:

Paying taxes on income you didn’t actually use, and then also

Paying capital gains taxes when you sell shares for cash, and/or

Paying ordinary income tax on withdrawals from IRAs and 401(k)s.

By spending the income you’re already taxed on, you reduce tax drag and keep more of your portfolio working for you.

Additionally, asset location — the strategy of placing tax-efficient investments in taxable accounts and tax-inefficient ones in IRAs — can further minimize your lifetime tax bill. (See my related blog post "Reduce Taxes Through Proper Asset Location" on this topic.)

The Bottom Line

Dividends and interest are not “extra” returns — they are part of your portfolio’s total return. When following the 4% Rule (or a similar safe withdrawal framework), understanding how that income fits into your total return — and how to use it efficiently — can make a significant difference in your after-tax outcomes.

A smart withdrawal plan is not just about how much you take; it is also about where the money comes from and how it is taxed. By utilizing proper asset location strategies, you can shield your bonds, dividend stocks, and REITs from taxes, allowing your portfolio to grow faster and your withdrawals to go further in retirement. Learn more about tax-efficient asset location and withdrawal strategies here and here.

If you want to optimize your withdrawal sequence, tax strategy, and income sustainability in retirement, consider building a personalized withdrawal plan that fits your portfolio, tax situation, and lifestyle goals.

Visit www.flourishingpathfinancial.com/book-online to schedule a free Discovery Session.

Author: John Macy, MBA, RICP®

John Macy is a professional financial coach and the founder of FlourishingPath Financial Coaching. With over six years of experience as a financial coach, John helps pre-retirees and retirees design resilient portfolios and income streams for their next act. Read his full story here.

Comments