Reduce Taxes Through Proper Asset Location

- John Macy

- Dec 10, 2025

- 3 min read

Updated: 2 days ago

Written by John Macy, Financial Coach, MBA, Retirement Income Certified Professional® (RICP)

Are your investments in the right accounts?

Let’s assume you have decided on your portfolio asset allocation (what proportion of your portfolio will be invested in stocks, bonds, real estate, commodities, etc.) and the specific investments you want to have in your portfolio. Great! But if you don't place them in the right type of account—Traditional IRA/401(k), Roth, or Taxable—you could be wasting money on taxes every year.

Asset location is the simple art of using the tax code to boost your portfolio’s after-tax return without taking on any extra risk.

Think of proper asset location as tax-efficiency for your portfolio — the art of placing the right investments in the right types of accounts to keep more of your returns working for you instead of going to the tax collector.

How Can You Reduce the Tax Drag on Your Portfolio?

Think of your portfolio like a car driving toward your financial goals. Taxes are like hitching a trailer (the IRS) to the back of your car — the lighter and more aerodynamic the trailer, the less it will slow down your progress. Fortunately, with a little bit of thought you can reduce the tax drag on your portfolio.

Different types of investments generate different kinds of income that are taxed very differently — some slow down your portfolio’s performance much more than others. Your goal is to use tax-advantaged accounts (Traditional and Roth) to reduce the tax drag for investments that generate the most taxable income.

Here is the ultimate guide to putting your assets in the right place:

Where Should Your Assets Live to Reduce Tax Drag?

1️⃣ Tax-Deferred Accounts (Traditional IRA, 401(k), etc.)

→ Traditional IRA/401(k) accounts provide tax-deferred growth. Placing your slower-growing and income-generating assets shelters them from current taxes and enables tax-deferred compounding, while recognizing that any assets will be taxed later at ordinary tax rates.

→ Best for tax-inefficient and slower-growth assets like:

✅ Taxable bonds

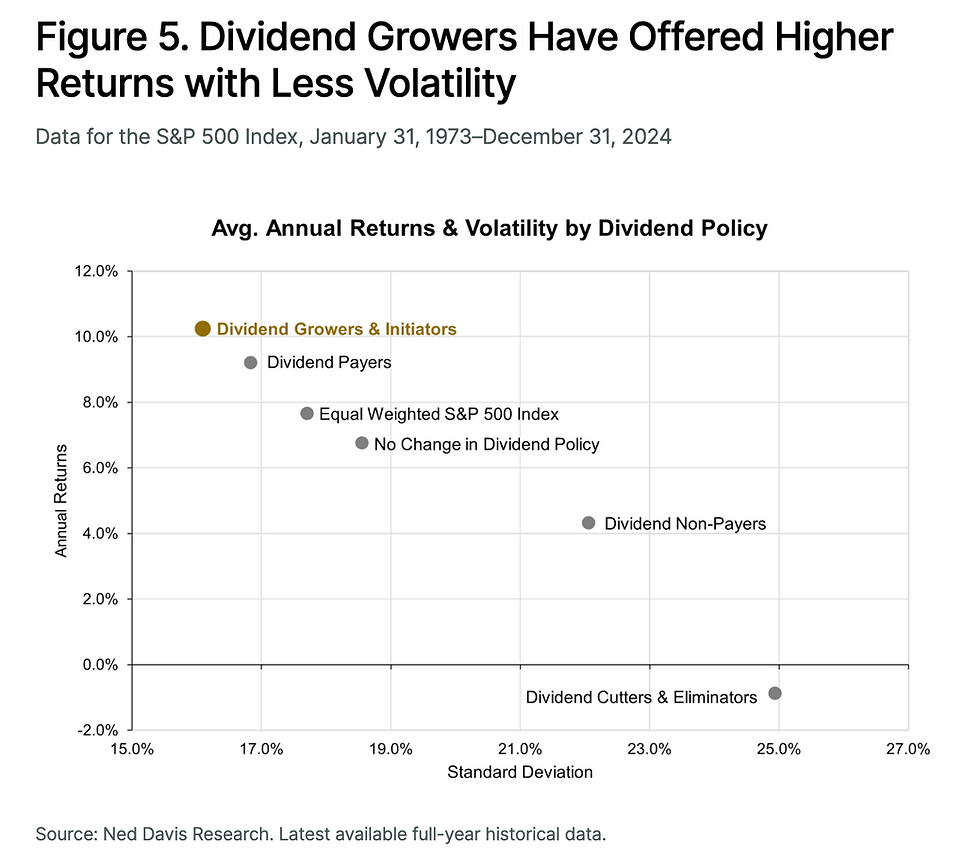

✅ Dividend stocks/ETFs (although, if qualified dividends could go in taxable)

✅ REITs (Real Estate Investment Trusts)

✅ Actively managed mutual funds

✅ TIPS (Treasury Inflation-Protected Securities) — TIPS generate 'phantom income'—taxable inflation adjustments you haven't received in cash yet—making them ideal for tax-deferred accounts.

2️⃣ Taxable Brokerage Accounts

→ Within taxable brokerage accounts, interest, dividends, and capital gains are taxed in the current year. However, qualified dividends and long-term capital gains are taxed at much lower rates than ordinary income, so taxable accounts can be just as efficient as Traditional IRA/401(k) accounts if the right assets are placed there.

→ Best for tax-efficient assets like:

✅ Lower-dividend-paying or qualified-dividend stocks

✅ Municipal bonds (interest is tax-free)

✅ Tax-managed index funds and ETFs

✅ Real estate investments that benefit from depreciation and other deductions

3️⃣ Roth Accounts (Roth IRA, Roth 401(k))

→ Roth accounts provide tax-free growth, so placing your highest-growth assets here maximizes the total dollar value of the tax exemption.

→ What should go here?

✅ Stocks or stock funds expected to grow the most over time

Summary Asset Location Recommendations

Tax Treatment | Asset Type | Preferred Account |

Most Tax-Inefficient | Taxable Bonds, Dividend Stocks, REITs, TIPS, Active Funds | Traditional IRA / 401(k) |

High Growth Potential | Aggressive Growth Stocks, Small Cap, Crypto | Roth IRA |

Tax-Efficient | Passive Index Stock ETFs, Municipal Bonds | Taxable Brokerage |

The Benefit Over Time

Proper asset location doesn't change your overall portfolio risk, but it can significantly change your after-tax return. By avoiding taxes on certain investment income year after year, the compounding effect can quietly add tens or even hundreds of thousands of dollars to your final retirement nest egg.

It's not just about what you invest in — it's about where you hold those investments.

Contact me or visit www.flourishingpathfinancial.com/book-online if you would like friendly, expert assistance with your financial planning.

Author: John Macy, MBA, RICP®

John Macy is a professional financial coach and the founder of FlourishingPath Financial Coaching. With over six years of experience as a financial coach, John helps pre-retirees and retirees design resilient portfolios and income streams for their next act. Read his full story here.

Comments