Are Bonds or Dividend Stocks the Better Income Strategy For Retirement?

- John Macy

- Dec 10, 2025

- 3 min read

Updated: 2 days ago

Written by John Macy, Financial Coach, MBA, Retirement Income Certified Professional® (RICP)

If you’re retired (or planning for it soon), you might be thinking: “Should I rely more on bonds or dividend-paying stocks for my retirement income?”

It’s a great question — and the answer depends on your goals, risk tolerance, and need for stability.

Let’s break it down.

Which Pays More Right Now?

Yields change over time — but in recent years:

Bonds (especially Treasuries or investment-grade corporates) have been paying around 4–5%, depending on maturity and risk.

Dividend-paying stocks often yield 2–4% — though some sectors (like utilities and Real Estate Investment Trusts (REITs) and Business Development Companies (BDCs)) often pay a bit more.

So bonds typically have a higher yield than stocks, but the risk and stability behind that income are very different.

Bonds: More Stability, Less Growth

Bonds are generally considered the “steady paycheck” of your portfolio. They pay legally-obligated interest on a schedule and give your principal back at maturity. They’re ideal for covering short- to mid-term spending needs and reducing portfolio volatility.

However, their interest payments are typically fixed, which means inflation steadily eats into their real value (purchasing power risk) over time (unless you buy inflation-protected bonds such as TIPS (Treasury Inflation Protected Securities)).

And remember, the market price of a bond is inversely related to prevailing interest rates in the market. So, if interest rates fall the market value of your bonds will rise, and if interest rates increase the market value of your bonds will fall. The dramatic increase in interest rates in 2022 illustrates this phenomena very well, as aggregate bond market prices fell 13-15% and long-term Treasury prices fell about 29%. So, while bonds are generally thought to be "safer" and less volatile than stocks, they can and periodically do suffer significant price declines. However, unless the borrower defaults on its debts, you will get your scheduled principal and interest payments.

Dividend Stocks: More Growth, More Risk

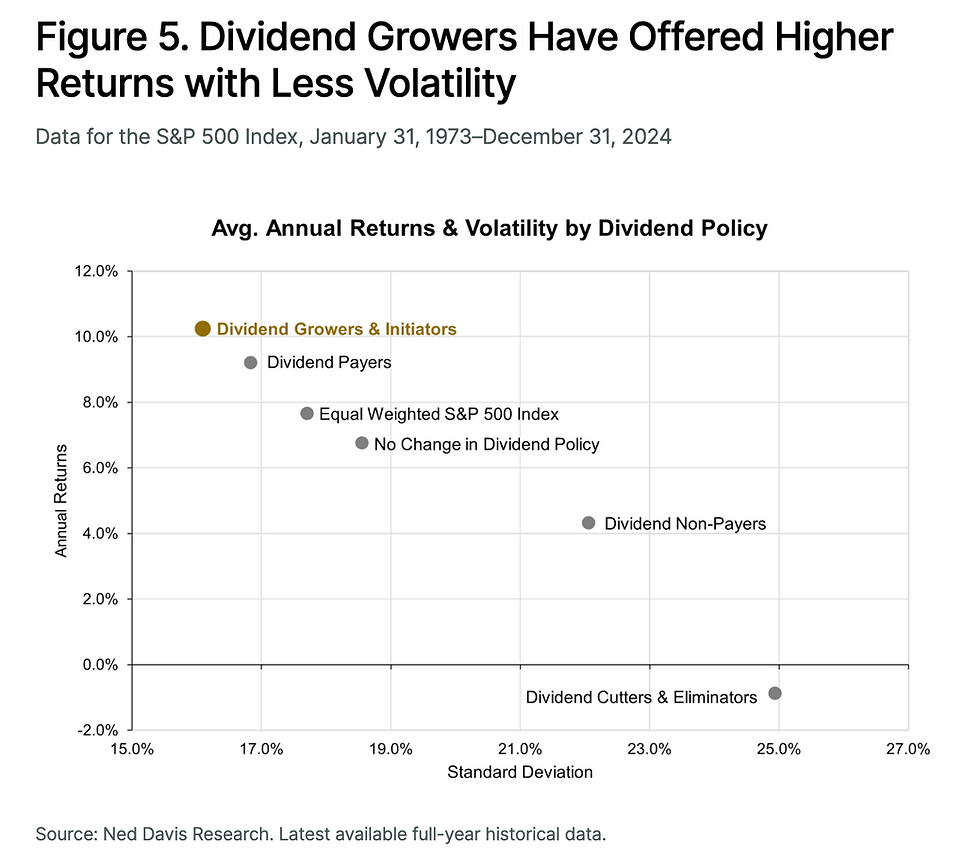

Dividend-paying stocks can offer rising income over time — because healthy companies often increase their dividends. That makes them powerful for long-term inflation protection.

But remember: dividends aren’t guaranteed. Companies can — and sometimes do — cut or suspend them when profits fall. That’s why diversification and focusing on high-quality companies (not just the highest yielders) is key.

Summary Comparison: Bonds vs Dividend Stocks

Feature | Bonds (Treasuries/Investment Grade) | Dividend-Paying Stocks |

Primary Goal | Capital Preservation & Stability | Long-Term Growth & Inflation Protection |

Income Type | Fixed Interest (Legal Obligation) | Discretionary Dividends (Can Grow or Be Cut) |

Inflation Hedge | Low (unless using TIPS) | High (Healthy companies raise dividends) |

Price Volatility | Lower (Prices move with interest rates) | Higher (Prices move with market sentiment) |

Historical Yield | Typically 4–5% (Current Market) | Typically 2–4% (Varies by Sector; some sectors like REITS, BDCs, and MLPs are higher) |

So Which Is Better?

For most retirees, the best answer is: a blend of both.

Bonds provide stability and predictable income.

Dividend stocks provide growth potential and inflation protection.

Think of bonds as your steady income engine and dividend stocks as your growth engine that keeps your retirement income rising over time. In addition to dividends, stocks will also usually provide some capital gains over time. A typical retiree portfolio will have a stock/bond mix of anywhere from 50%/50% to 70%/30%. Being too conservative and having too small an allocation to stocks can create problems with income sustainability in retirement due to limited ability to keep up with inflation.

Pro Tip

Avoid chasing the highest yielding stocks or bonds — that’s called the high dividend or yield trap. Those “too good to be true” yields often come from companies in trouble or sectors with higher risk of cuts. Focus instead on quality, consistency, and diversification.

The Bottom Line

You don’t have to choose either/or — there is magic in combining both into a balanced portfolio. You can also add some Master Limited Partnerships (MLPs), Real Estate Income Trusts (REITs), Business Development Companies (BDCs), preferred stock, and other types of assets for even greater diversification and income streams. A thoughtful mix of stable bond income and growing dividend income (plus some growth stocks) can give you a smooth cash flow today and a growing income stream that can survive decades of inflation. Total return (price appreciation + dividend/interest income) is ultimately what matters most in enabling your portfolio to survive for 30+ years in retirement.

Ready to design a blended portfolio that maximizes stability and growth for your retirement?

Let’s optimize your retirement income strategy. Send me a message or visit www.flourishingpathfinancial.com/book-online if you would like friendly, expert assistance in building your resilient retirement income plan.

Author: John Macy, MBA, RICP®

John Macy is a professional financial coach and the founder of FlourishingPath Financial Coaching. With over six years of experience as a financial coach, John helps pre-retirees and retirees design resilient portfolios and income streams for their next act. Read his full story here.

Comments