True Diversification: What Most DIY Investors Get Wrong About Building a Portfolio

- John Macy

- 4 days ago

- 8 min read

Updated: 2 days ago

Written by John Macy, Financial Coach, MBA, Retirement Income Certified Professional® (RICP)

Introduction

Many investors believe they are diversified because they own several mutual funds, a handful of ETFs, and perhaps a few individual stocks.

But true diversification isn't about how many investments you own. It's about owning investments that respond differently to economic events.

If all of your holdings tend to rise and fall together, you may have more concentration risk than you realize.

|

The purpose of diversification is not to maximize returns in every market environment. Rather, it is to increase the likelihood that some portion of your portfolio is performing well when another portion is struggling.

In this article, we'll explore what diversification really means, how different asset classes behave, and how DIY investors can build more resilient portfolios.

Understanding Correlation

One of the most useful tools for evaluating diversification is a concept called correlation.

Correlation measures how closely two investments move together.

+1.0 Correlation: Assets move together almost perfectly.

0 Correlation: Assets move completely independently.

-1.0 Correlation: Assets move in completely opposite directions.

Many investors assume they need investments with negative correlations. While that can be helpful, the real goal is often to combine assets with low or modest correlations that also have positive long-term expected returns.

For example:

U.S. Stocks and International Stocks are positively correlated but not identical.

Stocks and Bonds often have low correlations (but not always).

Managed Futures have historically exhibited very low correlations to stocks.

Gold frequently responds to different economic forces than stocks and bonds.

When assets respond differently to economic events, the investor's overall portfolio may experience smaller drawdowns, a smoother investment journey, and potentially higher total returns over time.

Why Diversification Matters

Consider the following environments:

Economic growth

Recession

Inflation

Deflation

Rising interest rates

Falling interest rates

Geopolitical uncertainty

No single asset class performs best in every environment.

Stocks may thrive during periods of economic growth.

Bonds often perform well during recessions and deflationary periods, especially when interest rates decline.

Gold may shine during monetary uncertainty.

Managed futures have historically performed well during some of the most challenging market environments.

Since nobody can really predict the future, diversification helps ensure that your financial future isn't dependent on a single economic outcome.

Research Supports the Importance of Alternatives

The original research that demonstrated the benefits of diversification in a portfolio was done by famed economist Harry Markowitz in 1952 (for which he later earned a Nobel Price in Economics). His research, known as Modern Portfolio Theory, described something known as the Efficient Frontier. The most important conclusion from the research is that by combining non-correlated investments (just common stocks in his original research) — assets that don't move in perfect lockstep — you can structurally (and significantly) reduce overall volatility without sacrificing performance. Alternatively, you can improve performance without increasing volatility. The Efficient Frontier is a curve that shows the combinations of portfolios that offer the absolute best risk-adjusted return profile.

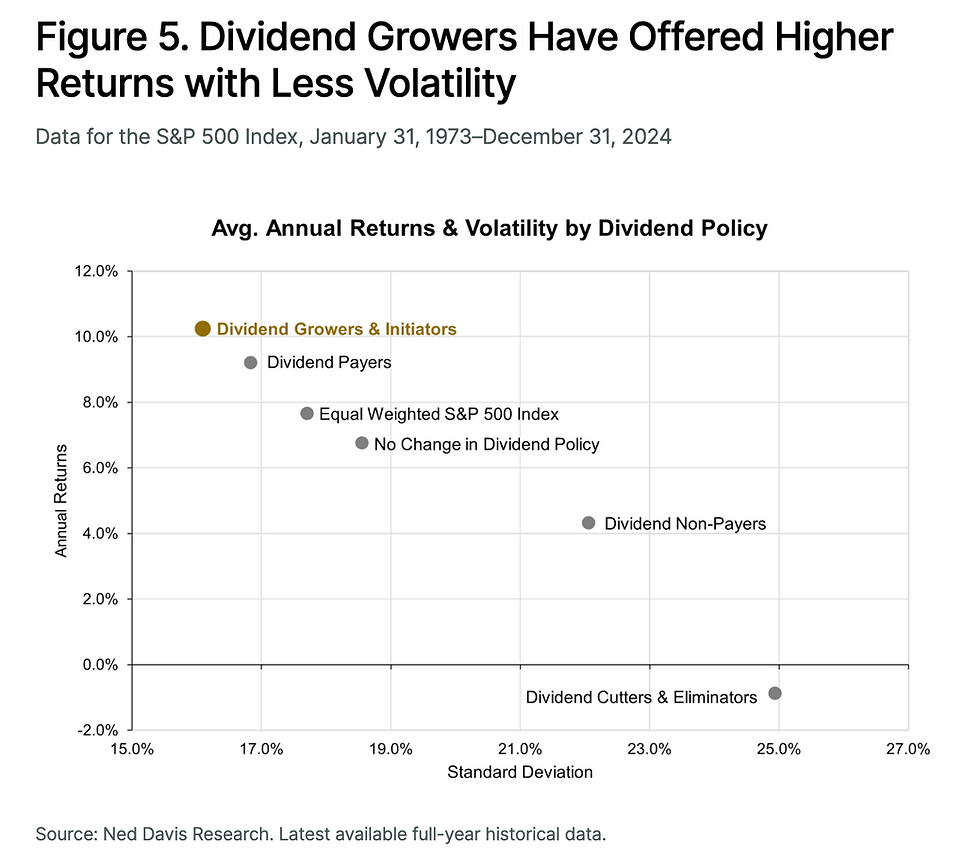

More recently several investment firms such as Morgan Stanley and BlackRock have conducted additional research on the benefits of including alternative investments (other than common stocks) in a portfolio. See, for example, the chart below (from BlackRock Systematic) that shows how both risk and return are improved by adding alternative investments to a portfolio of stocks and bonds.

A Simplified Menu of Asset Classes

Stocks

Stocks represent ownership in businesses and have historically been one of the best long-term wealth-building assets. However, they are somewhat volatile and in periods when market sentiment is poor they can decline 20-50%.

Examples include:

Global Stocks (VT, ACWI)

U.S. Stocks (VTI, ITOT)

International Developed Stocks (VEA, IEFA)

Emerging Markets (VWO, IEMG)

Bonds

Bonds provide income and have historically helped reduce portfolio volatility in most years (1931, 1969, 1973, 1977, and 2022 were big exceptions). Note that when traditional stock and bond diversification breaks down simultaneously under inflationary pressures, in addition to having more true diversification from other asset categories, having an established retirement income floor prevents you from being forced to sell equities at a loss.

Examples include:

Total Bond Market (BND, AGG)

Intermediate Treasuries (VGIT, SCHR)

Long-Term Treasuries (VGLT, TLT)

Treasury Inflation-Protected Securities (SCHP, TIP)

Real Estate

Real estate can provide income, inflation protection, and modest diversification.

Examples include:

Public REITs (VNQ, SCHH)

Global REITs (REET, VNQI)

Investors may also gain exposure through private real estate funds, syndications, or direct ownership of rental properties. These are less liquid but tend to be less volatile than publicly-traded REITs.

Gold and Commodities

Gold and commodities often respond differently than stocks and bonds. Many investors use them as inflation hedges and crisis diversifiers.

Examples include:

Gold (IAU, GLDM, GLD)

Broad Commodities (PDBC, COM)

Managed Futures

Managed futures are systematic strategies that follow market trends across stocks, bonds, currencies, and commodities. Because they can profit from both rising and falling markets, they have historically provided valuable diversification during major market crises.

Examples include:

DBMF

CTA

KMLM

Many investors have never heard of managed futures, yet research from Cliff Asness, Antti Ilmanen, Kathryn Kaminski, and others has consistently identified trend-following managed futures as one of the most effective diversifiers to a stock portfolio.

While managed futures can experience long periods of underperformance, they have historically demonstrated:

Low correlation to stocks

The ability to profit during prolonged market declines

Strong performance during some inflationary environments

Potential "crisis alpha" during major market disruptions

For investors seeking diversification beyond traditional stock and bond portfolios, managed futures may be worth exploring. Adding 10-20% managed futures to a portfolio can noticeably reduce portfolio volatility while potentially improving overall total return (over a multi-year time horizon).

Private Credit and Private Equity

Examples include:

Private Credit

Publicly traded Business Development Companies (BDCs) such as ARCC, HTGC, MAIN, and TSLX

Private credit funds available to accredited investors

Private Equity

Private equity partnerships

Listed alternatives such as PSP (though not a perfect proxy)

These investments may offer higher return potential but generally involve less liquidity, greater complexity, and longer holding periods.

Long-Term Correlation Snapshot

The table below provides illustrative long-term correlations among major asset classes. Note: If viewing on a mobile device, scroll horizontally to view the full correlation matrix

Asset Class | U.S. Stocks | Int'l Stocks | Bonds | Real Estate | Commodities | Managed Futures | Private Credit |

U.S. Stocks | 1.00 | 0.78 | 0.20 | 0.65 | 0.35 | -0.05 | 0.65 |

Int'l Stocks | 0.78 | 1.00 | 0.15 | 0.60 | 0.42 | -0.02 | 0.58 |

Bonds | 0.20 | 0.15 | 1.00 | 0.15 | -0.10 | 0.25 | 0.25 |

Real Estate | 0.65 | 0.60 | 0.15 | 1.00 | 0.25 | 0.05 | 0.50 |

Commodities | 0.35 | 0.42 | -0.10 | 0.25 | 1.00 | 0.18 | 0.30 |

Managed Futures | -0.05 | -0.02 | 0.12 | 0.05 | 0.18 | 1.00 | -0.08 |

Private Credit | 0.65 | 0.58 | 0.25 | 0.50 | 0.30 | -0.08 | 1.00 |

Illustrative long-term estimates. Correlations change over time and often increase during periods of market stress. The lower the correlation (or negative) the better able an asset class is to diversify your portfolio.

Which Assets Tend to Thrive in Different Economic Climates?

Economic Climate | Stocks | Bonds | Gold | REITs | Managed Futures |

Sunny Growth ☀️ | ● | ◔ | ○ | ◕ | ◔ |

Recession 🌧️ | ○ | ● | ◑ | ◔ | ◕ |

Inflation 🔥 | ◔ | ○ | ◕ | ◑ | ● |

Deflation ❄️ | ◔ | ● | ◔ | ◔ | ◑ |

Crisis ⚡ | ○ | ◕ | ◑ | ○ | ● |

What Are the Best Diversifiers?

Research from investors and academics such as Cliff Asness, Antti Ilmanen, Kathryn Kaminski, and Andrew Lo suggests that some diversifiers have historically been more effective than others.

Asset Class | Diversification Benefit |

Managed Futures | Excellent |

Treasury Bonds | Very Good |

Gold | Good |

Commodities | Good |

Real Estate | Moderate |

Private Credit | Moderate |

Private Equity | Limited |

Additional U.S. Stock Funds | Low |

Three Portfolio Approaches for DIY Investors

Portfolio Approach Tier 1: The Simple Global Portfolio

Best For: Investors seeking simplicity, low costs, and minimal maintenance.

Example Allocation:

60% Global Stocks (VT)

30% High-Quality Bonds (BND or AGG)

10% Gold (IAU or GLDM) or Real Estate (VNQ)

Option A: Real Estate

Real estate may appeal to investors who:

Prefer income-producing assets

Want inflation protection

Believe in the long-term value of real estate ownership

Trade-off: Public REITs often behave similarly to stocks during major market declines.

Option B: Gold

Gold may appeal to investors who:

Want a potential crisis hedge

Are concerned about inflation or currency debasement

Seek an asset that behaves differently than stocks and bonds

Trade-off: Gold generates no income and has historically produced lower long-term returns than stocks.

Some investors choose a middle ground:

5% Gold

5% Real Estate

Portfolio Approach Tier 2: The Enhanced Diversification Portfolio

Best For: Investors who want additional protection against inflation, market shocks, and changing economic environments, provided they are willing to have a slightly more complicated portfolio.

Example Allocation:

50% Global Stocks (VT)

20% Bonds (BND or AGG)

10% Managed Futures (DBMF, CTA, or KMLM)

10% Commodities (PDBC)

10% Real Estate (VNQ)

This portfolio introduces additional return drivers beyond traditional stocks and bonds.

Portfolio Approach Tier 3: The Endowment-Inspired Portfolio

Best For: Experienced investors with larger portfolios and longer time horizons.

Example Allocation:

40% Global Stocks (VT) with optional tilts to Value (AVUV, DFSV) and International Value (AVDV)

15% Managed Futures (DBMF, CTA, KMLM, or private hedge funds)

15% Private Credit (private funds or publicly traded BDCs such as ARCC, HTGC, MAIN, and TSLX)

15% Private Real Estate or Private Equity

10% Gold (IAU, GLDM) and other real assets

5% Opportunistic Investments

This approach is loosely inspired by institutional portfolios such as Yale's endowment model and seeks to diversify across multiple economic drivers.

The Biggest Diversification Mistake

One of the most common mistakes investors make is confusing the number of investments they own with true diversification. Owning 500 stocks (or 5,000 stocks) is not necessarily better than owning 30-50 stocks.

A portfolio of:

20 technology stocks

5 U.S. stock ETFs (consisting of hundreds or thousands of stocks)

3 growth mutual funds (consisting of hundreds or thousands of stocks)

is less diversified than a portfolio consisting of:

Global stocks

Bonds

Real estate

Gold

Managed futures

Often, the greatest diversification benefits come from owning assets with fundamentally different return drivers. The goal is not simply to own more investments. The goal is to own investments that behave differently when markets become challenging.

Final Thoughts

No portfolio will outperform in every environment. And with a diversified portfolio you are virtually guaranteed to have something in your portfolio that is not performing as well as you would like in most years - some things will be up while other things will be down.

The purpose of diversification is not to maximize returns in every year. It is to increase the odds that your portfolio can survive inflation, recessions, bear markets, rising interest rates, and unexpected economic shocks, while thriving when market conditions are good. It is also to improve the overall risk-adjusted returns of your portfolio.

|

Ready to Build a More Resilient Portfolio?

If you'd like help evaluating your current asset allocation, understanding diversification opportunities, or building a portfolio aligned with your goals and risk tolerance, I'd love to help.

Visit www.flourishingpathfinancial.com to learn more about FlourishingPath Financial Coaching and schedule a complimentary introductory conversation.

Note: the examples provided in this article are for education purposes only. They are not specific recommendations for any particular investor. All investors should determine their objectives, time horizon, and risk preferences/tolerances, do their own careful due diligence, and make an informed decision about how to construct their portfolios and which investments to select that fit their objectives.

Author: John Macy, MBA, RICP®

John Macy is a professional financial coach and the founder of FlourishingPath Financial Coaching. With over six years of experience as a financial coach, John helps pre-retirees and retirees design resilient portfolios and income streams for their next act. Read his full story here.

Comments